The California regulator has declared bankrupt Silicon Valley Bank (SVB), the 16th largest US bank. The credit organization was focused on start-ups.

Silicon Valley Bank was very closely tied to the finances of technology companies, and it is unlikely that its problems will spill over to the rest of the banking sector, as happened in the months leading up to the "Great Recession" more than a decade ago. The largest banks in the country, which are more likely to become a source of systemic economic problems, are doing well with balance sheets and capital today.

Nervousness in the banking sector continued throughout the week, and the Silicon Valley bankruptcy sent shares of nearly every financial institution lower on Friday, already down double digits since Monday.

The collapse of Silicon Valley happened at an incredible rate. Some industry analysts said as early as Friday that this is a good company and a smart investment. The management of the bank on Friday morning tried to raise capital and find additional investors. However, trading in the bank's shares was suspended before the start of the trading session on Wall Street due to extreme volatility.

The era of startups is coming to an end and is moving into hyperconcretion mode. Everything you do will be copied immediately! No one else will allow a startup to slowly and systematically develop and gain critical mass.

Traditional business valuation systems do not work. Neither revenue, nor growth rate, nor brand, nor customer loyalty, nor unique offer matter anymore, because. are temporary and short term. Everything is on the line! Either you instantly occupy the market and destroy competitors in one fell swoop, or you will sink into oblivion.

The new conditions require different approaches to evaluation, financing and development strategies. Venture capital funds are turning from a money bag into competence centers. The main qualities are: understanding of future markets, a network of competent contractors, well-established interaction processes, and a well-built infrastructure. Product strategy becomes the only competitive advantage!

The venture industry is flawed and inefficient, the race for innovation is nothing but a fake, and the current product approaches are a sham. The epic collapse of the SVB is just the beginning of the demise of the world's economic systems. Amen!

The collapse of Silicon Valley Bank: how and why the main bank of techno startups in Silicon Valley burst

Bankruptcy was the second largest in history among American commercial banks. In this article, we will try to understand what happened and how it can affect all of us.

Laura Izurieta, head of risk at Silicon Valley Bank, prudently resigned from the bank back in April 2022, and they couldn’t find a person for her position for almost a year (coincidence? I don’t think!)

Laura Izurieta, head of risk at Silicon Valley Bank, prudently resigned from the bank back in April 2022, and they couldn’t find a person for her position for almost a year (coincidence? I don’t think!)

How it all began: a bank for the geeky Zuckerbrins

40 years ago (in 1983) a bank appeared in California that made a bet on startups - it decided to serve mainly big-headed guys who created new promising businesses and raised a lot of money from venture investors.

Given that the business took place exactly in Silicon Valley, and the bank was called Silicon Valley Bank (SVB), this business model turned out to be extremely successful. After all, Silicon Valley has become a real cradle for fast-growing technology companies, which for the next few decades rowed money literally with a shovel (and some of it, of course, put it in the bank).

They say that Bob Medearis came up with the idea to drink Silicon Valley Bank while playing poker with another co-founder of the bank, Bill Biggerstaff. They had a good all-in, I must say!

They say that Bob Medearis came up with the idea to drink Silicon Valley Bank while playing poker with another co-founder of the bank, Bill Biggerstaff. They had a good all-in, I must say!

In 2020-2021, the technology industry in the United States experienced another boom: under the slogan of combating covid, unprecedentedly huge amounts of money were thrown into the financial system, and a significant part of it went precisely to finance “fashionable” fast-growing tech companies. The Nasdaq-100 index has almost doubled in these two years, and startups raced to conduct initial public offerings (IPOs) and raise money directly from venture capital investors on an industrial scale.

Not surprisingly, the business of SVB, which serves all these tech startups, also grew by leaps and bounds. Its client deposits more than tripled over that period (as did the bank's stock price) to reach roughly $200 billion by early 2022, making Silicon Valley Bank the 16th largest bank in the US (and second in California).

As they say - nothing foreshadowed trouble ...

As they say - nothing foreshadowed trouble ...

Any bank, of course, is happy when they bring a lot of money to it. But with big bucks comes a big responsibility: you have to decide where to invest them so that they earn a nice profit in the pocket of the owners of this bank. And this is where it gets interesting!

What to do with the money, Lebowski?

The classic business model of any bank is to collect more deposits at a lower rate, and distribute this money to reliable companies in the form of loans at a higher rate. In the case of Silicon Valley Bank, this turned out to be a little problematic: most of your startups from Silicon Valley do not look much like "safe businesses" (the guys there mostly have beautiful pictures with the promise of explosive revenue growth in the future - and not stable cash flows and strong collateral ). And they didn’t have much of a shortage of money: as I wrote above, in 2020–2021. except that investors didn’t line up in a queue to fill such startups with loot literally in bags.

Therefore, SVB decided that the money would be logical to invest in the stock market. No, of course, they did not go to buy Tesla shares with leverage - that would be too much. But to buy reliable bonds from the US government (US Treasuries), or mortgage-backed debt securities with suitable collateral in the form of real estate - why not?

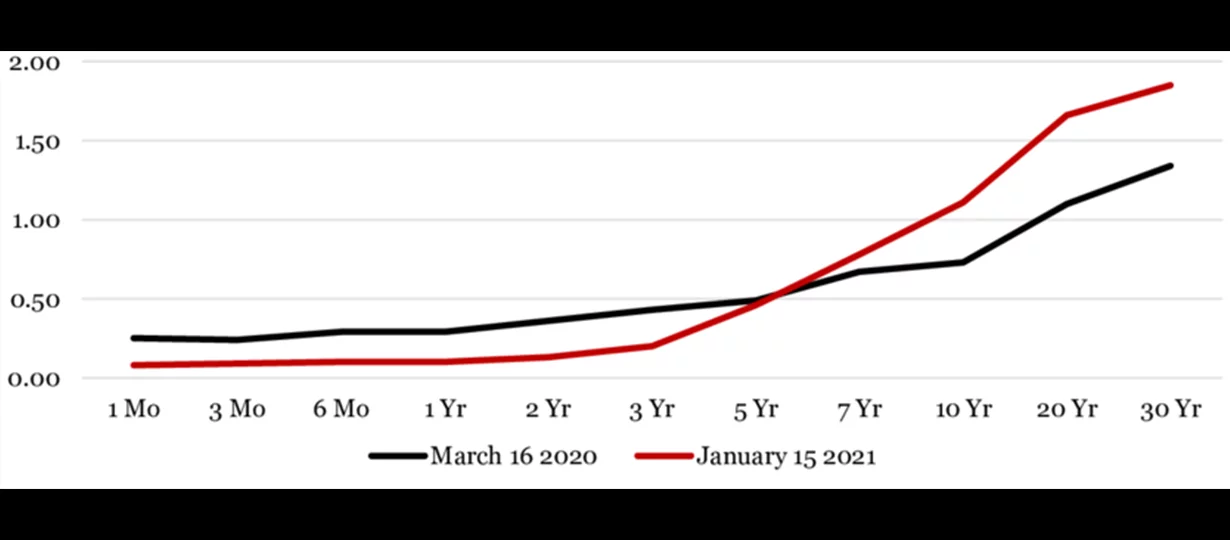

And now let's remember what yields gave reliable dollar bonds during that period:

Yield on U.S. government bonds as a percentage (vertical scale) depending on their maturity (horizontal scale) in 2020-2021 (source)

Yield on U.S. government bonds as a percentage (vertical scale) depending on their maturity (horizontal scale) in 2020-2021 (source)

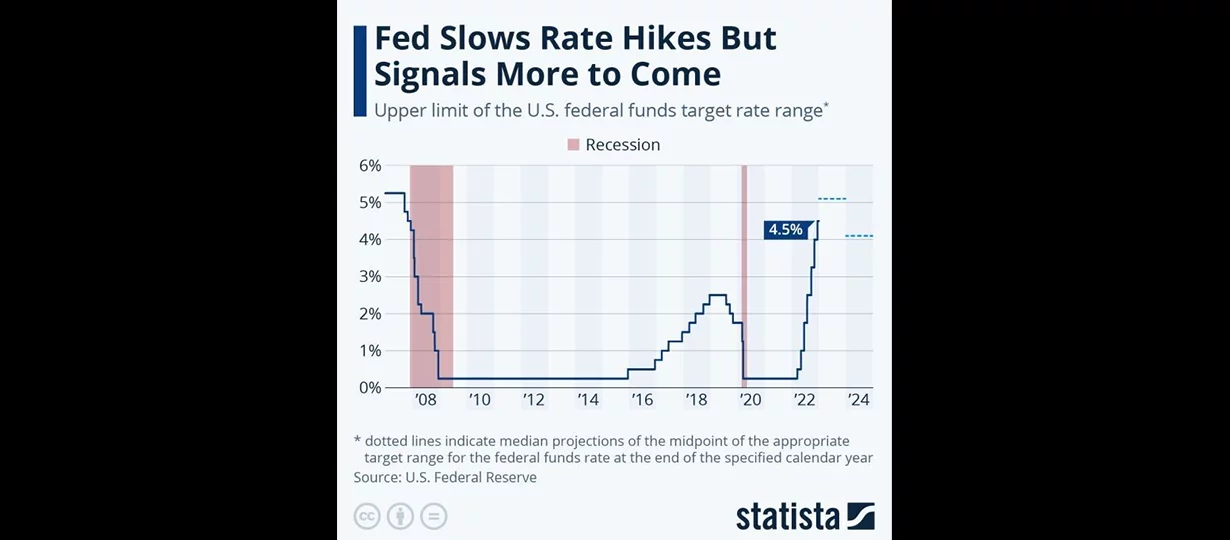

The US Federal Reserve then drowned the interest rate to almost zero (in the name of saving the economy from covid horrors), so placing money in reliable US Treasuries on the horizon of a year or two brought about zero profitability.

So the bankers from Silicon Valley Bank thought that by investing at 0% you won’t earn much for bread and butter (and they still have to pay all current expenses: salaries to employees, office rent, and so on). The solution was simple - the bankers simply dumped the lion's share of available funds into longer bonds with a maturity of 5-10 years (mostly mortgages), which at that time had a yield slightly above 1.5% per annum. Despite the fact that they paid almost no profitability to their clients on attracted deposits - a good margin, right?

How rising rates killed bonds

Any financier knows that when you buy long bonds, you take on the risk of rising interest rates. If you bought a long bond during a period of low rates, and then rates skyrocketed, then, in Tommy's terms from the movie Snatch, "You are PROPER FUCKED."

Long bond investor face expression in 2022

Long bond investor face expression in 2022

Why is this happening? Invisible hand of the market, ept! Follow the logic: suppose a company issues a $100 par value bond with a 1% coupon (which was the market level at the time), maturing in 50 years, and you buy it. A year later, the market level of rates increased, and now it is customary to lend to such companies already at 2% per annum.

Can you sell your bond to someone for $100? Of course not - you will not find such fools (why would someone invest at 1% when the market already gives 2% with a similar reliability?). But for a conditional $50, such a bond will be bought from you without any problems: after all, then a coupon of $1 per year will just give a yield of 2% on the “current market value” of the paper at $50 (the exact numbers will not be exactly the same, but these are the details - you understand the logic) .

In fact, this is exactly what happened in 2022: the head of the US Federal Reserve got a little crazy from the explosive growth of inflation, and at a record pace raised the interest rate from about zero to almost 5% (at the moment).

Surprise, motherfucker: the stock market has been bleeding non-stop for the whole of 2022 precisely because of the sharp increase in the Fed rate

Surprise, motherfucker: the stock market has been bleeding non-stop for the whole of 2022 precisely because of the sharp increase in the Fed rate

It is clear that in this situation, the bond portfolio of Silicon Valley Bank “sad”: by the 4th quarter of 2022, it showed a drawdown from 9 to 17%, which already, as it were, exceeded the size of the bank’s own capital (that is, the difference between existing assets and liabilities to contributors).

Bank run: why it's sometimes important to be first in line, not last

It is interesting that in itself this loss has not yet been fatal for the bank - after all, cunning accounting standards allow it to be partially not recognized immediately (more details here). And there is even logic in this: because of the growth in rates, the bonds, as it were, sink not forever, but temporarily. If you hold them until maturity, then they will recover over time and everything will be ok.

But this logic only works if the bank has "the ability to wait." And here is the time to remember that most of the deposits in Silicon Valley Bank are the so-called “demand deposits”, which can be withdrawn at any time. Oops...

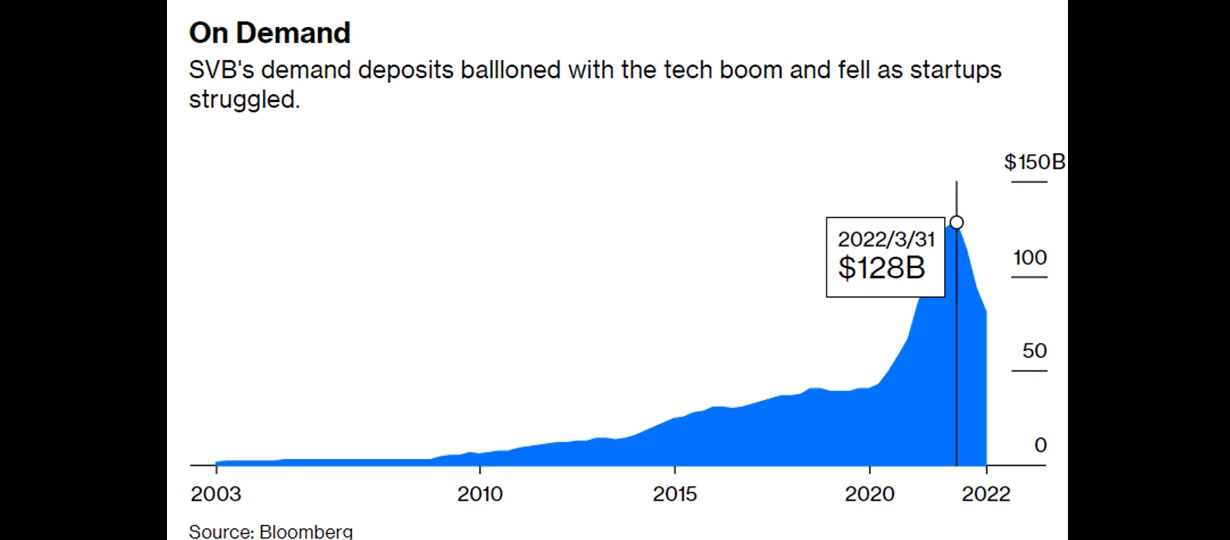

Bloomberg: By March 2022, SVB had accumulated almost $130 billion in demand deposits - and by the end of the year, $50 billion of them the smartest clients preferred to take

Bloomberg: By March 2022, SVB had accumulated almost $130 billion in demand deposits - and by the end of the year, $50 billion of them the smartest clients preferred to take

The systematic outflow of such deposits from the bank began in mid-2022. And there is no malicious intent on the part of Silicon Valley Bank customers: the tech industry began to decline, it was no longer easy to attract new investors' money, so many companies began to actively “eat up” the previously accumulated reserves.

But for SVB, this felt like a gradual activation of a time bomb: after all, deposits on demand had to be reimbursed from the most liquid assets, which meant that more and more strongly sagging long-term bonds remained on the balance sheet. And the faster the outflow of deposits became, the clearer it became that simply “sitting out to maturity” in these bonds would not work - sooner or later they would have to be sold at a loss in order to receive funds to return money to customers right now.

Actually, this is exactly what happened, and in 2023 the bank had to start selling these ill-fated long bonds at a loss - and then it suddenly became very clear to everyone that “the king is naked”, and in fact there will not be enough money for everyone. Venture start-ups from Silicon Valley began vying to call each other and advise urgently to remove all the loot from Silicon Valley Bank. But it was too late...

In finance, this phenomenon is called "bank run", and it looks something like this, yes

In finance, this phenomenon is called "bank run", and it looks something like this, yes

It turns out that here the concentration of SVB in one sector played a cruel joke on the bank: if they had many small retail clients, they might have passed. But since IT startups in the Valley communicate very closely with each other, there was a full run on the bank, when everyone tries to get their money out early (because the last one in this line may not get anything).

Well, and a logical result - on March 10, banking regulators in the United States began, de facto, the bankruptcy procedure for SVB.

Bankruptcy of the largest bank in California: little pleasant

All transactions with the bank were instantly suspended - for a huge number of startups from the Valley, this was a real shock (many of them used Silicon Valley Bank as the only place to store funds raised from investors).

The American deposit insurance system FDIC is already promising to start paying out affected depositors next week, with the insured amount amounting to $250,000 per deposit. But this is only a part of the funds, in the region of 15% of the total amount of deposits. What will happen to the rest of the contributors is still unclear.

The worst case is if the case ends in a full-fledged bankruptcy, with the gradual sale of all assets and the division of the resulting pile of money among everyone to whom the bank owes. This process will most likely not be quick - but, nevertheless, investors should eventually receive the principal amount invested back (I think at least 80% - but it will be possible to say for sure only on the basis of detailed up-to-date financial statements).

A good scenario assumes that someone big will buy the whole bank and close the hole in the balance sheet with their own funds, getting a working business in return (which was estimated quite well by the market a year ago).

It is clear that US regulators will do their best to drown for a "good" scenario - so that all the people around them get what is due to them, calm down, and the negative effects on the mood prevailing among financiers are limited. But even in the worst-case scenario, so far it looks like the bankruptcy of a bank even of this size is unlikely to cause the beginning of the collapse of the entire financial system according to the domino principle (and this, of course, in such situations, everyone fears the most).

It hurts the most, it seems, as usual, hit the cryptans

In Silicon Valley Bank, not only classic IT entrepreneurs kept money, but also cryptans. In particular, the company Circle, which manages one of the largest USDC stablecoins, also kept part of the reserves for this token there. So, in the wake of such news, USDC cheerfully depegged on the night from Friday to Saturday (disconnected from $1) and is currently being traded in different places for about 90% of the face value.

TradingView: USDC depeg at its finest – USDC is currently valued at around 90 cents per dollar on the exchange

TradingView: USDC depeg at its finest – USDC is currently valued at around 90 cents per dollar on the exchange

Why at the moment everyone in a panic gets rid of USDC and dropped the price a lot - this is understandable; but let's try to figure out what situation we are in in terms of the fundamental indicators of the security of this stablecoin.

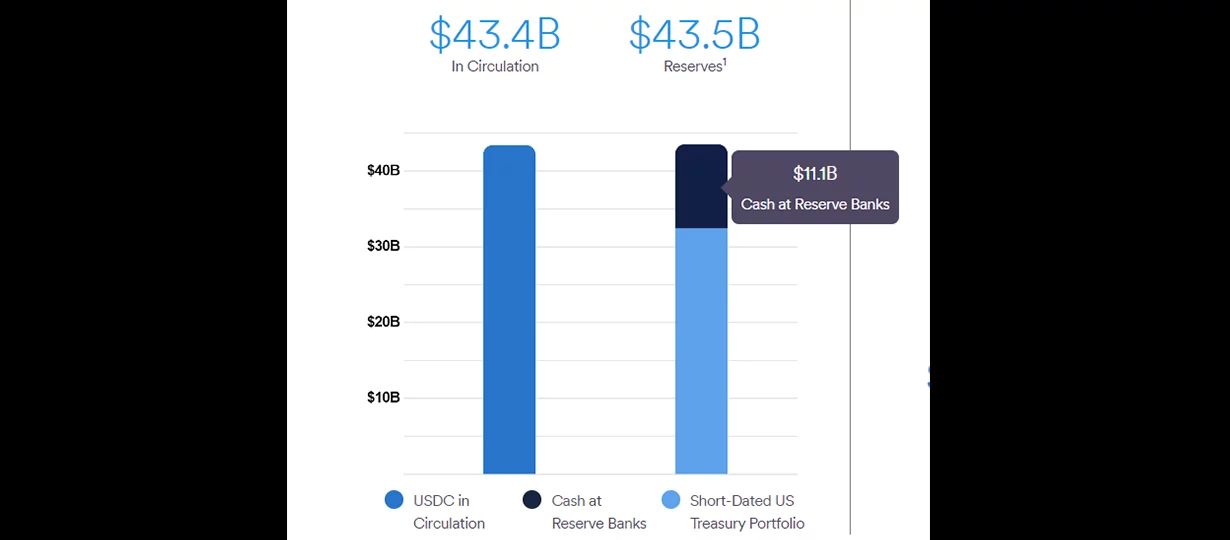

According to the latest data from the Circle website, as of March 9, total reserves amounted to an impressive $43.5 billion, of which 75% ($32.4 billion) was short-term US government debt - about these funds, pah-pah, you don’t seem to worry. But $ 11 billion lay in bank accounts, and according to Circle on Twitter, $ 3.3 billion managed to end up in Silicon Valley Bank.

Circle: As of March 9, the company's website shows that deposits in US banks represent approximately 25% of all USDC reserves.

Circle: As of March 9, the company's website shows that deposits in US banks represent approximately 25% of all USDC reserves.

If we take it “on the forehead”, then the funds blocked on SVB accounts amount to 7.5% of the reserves, which is a lot. But at the same time, as we discussed above, it is hardly worth considering this money as “completely missing”. If we assume that at least 80% of the bank's liabilities are adequately backed by assets, then the real "hole" in Circle's balance sheet can be only ~1.5%, which already does not look so threatening. Taking into account the fact that now reliable short US Treasuries bring 5% per annum, it is possible to recoup this amount purely from interest income in four months.

True, if everyone rushes en masse to exchange their USDC for real cash directly in Circle, then this “little hole” may begin to grow ... And the last one who comes for such an exchange will already get a donut hole - in fact, because the outcome and these same raids on banks take place (and Circle in this case acts as a kind of crypto-bank).

Is it likely? I am not here to give advice and predictions - but I can share my personal opinion: it seems to me that with the beginning of the next working week (when interbank transfers and other things start working again), arbitrageurs should quickly return the USDC peg to $1 (albeit not ideally, but a deviation should be reduced from 10% to at least 1-2%). At the same time, we should expect a significant reduction in USDC capitalization due to the work of arbitrageurs (who will buy tokens at $0.9 and exchange them in Circle for a real crunchy dollar).

So one of the main questions here is whether Circle will have enough patience and infrastructural capabilities to sit out the first wave of outflow of funds, and how much they will be able to draw a clear and transparent picture for cryptans regarding “what is with the reserves now and what is the plan for the future.”

I think this is the face Jeremy Aller (CEO Circle) is looking forward to starting the next work week with.

I think this is the face Jeremy Aller (CEO Circle) is looking forward to starting the next work week with.

A worse scenario for USDC crypto-holders here might look something like this: Circle says “sorry, there is a hole in the balance, so we are suspending the exchange of USDC for dollars - until we figure out how to fairly share the rest of the reserves among everyone.” Based on our calculations above, this in itself will not mean that all the money in USDC is lost (Circle has a lot of real assets), but all arbitrage mechanisms will break down at the moment - and USDC quotes will go even much lower than $0.9.

In general, we'll see. It is not an investment recommendation, but personally I still bet on a moderately positive scenario for USDC - and I’m getting ready on Monday-Tuesday, if quotes again approach $1, to slowly diversify my “crypto pillow” away from USDC. But, of course, I could be wrong.

P.S. I foresee a lot of gloating in the comments on the topic that “Tether was branded for unreliability, but USDC ended up well!” Well, here we must also take into account that we now know about the problems of USDC precisely because of the greater transparency of this token. If Tether got into the same situation, we would most likely simply not even know about it now (and, accordingly, it’s not a fact that the situation inside the reserves is now much better).

Elon Musk reacts in his own style, launches a wave in the direction he needs. And hints that he is open to the idea of buying Silicon Valley Bank.

If the material turned out to be useful to you, I will be grateful for subscribing to my TG channel